Why Enterprises That Master Stablecoins in 2026 Will Outrun Everyone Else?

January 8, 2026

share

share

The stablecoin market entered 2026 with $312 billion in total market capitalization, but the real story lies beneath the surface. While USDT ($187B) and USDC ($75B) continue to dominate with 84% combined market share, an unprecedented wave of businesses, from national banks like SoFi to payment giants like PayPal, Fiserv and even state governments like Wyoming, are launching proprietary stablecoins. This is a huge fundamental shift in how businesses now view stablecoins as an infrastructure that generates revenue and enables entirely new business models.

This article explores the imperatives driving these stablecoin launches, the revenue models that make them profitable, the on-chain metrics that proves they have the desired traction, and the emerging ecosystem of stablecoin centric businesses. We expect this will be a modest start for builders who are looking to capture the stablecoin opportunity in 2026.

When businesses issue fiat-backed stablecoins at 1:1 parity, they hold equivalent reserves in U.S. Treasury Bills or bank deposits, earning substantial yields while users hold zero-yield tokens. This creates a massive arbitrage opportunity that requires no transaction fees.

Tether, for example, earned $5.2 billion from reserve interest in the first half of 2024 alone, with profits exceeding $10 billion in Q1-Q3 2025. The company now holds $135 billion in U.S. Treasury exposure, making it one of the largest holders of government debt globally. Circle (USDC) generated $711 million (96% of total revenue) from T-bill yields on $74 billion USDC in Q3 2025 alone.

The GENIUS Act’s requirement for 100% backing in U.S. Treasuries or cash has institutionalized this model. Stablecoin issuers collectively held $155 billion in U.S. Treasury Bills as of October 2025, which is 2.5% of outstanding T-Bills. Projections indicate this could grow to $1 trillion by 2028, potentially saving the U.S. government $114 billion annually in borrowing costs by creating automatic demand for government debt.

This is a major driver. It locks an user into a business ecosystem rather than converting to competitors.

PayPal’s PYUSD, for example, embeds into Venmo peer-to-peer payments and merchant checkout APIs. This enabled programmable money for automated recurring payments and ensured users stay within PayPal’s financial infrastructure. The company offers up to 4% rewards on held PYUSD, which creates additional stickiness.

SoFi Bank launched SoFiUSD on December 18, 2025, as the first OCC-regulated national bank to issue a stablecoin on a public blockchain. Rather than capturing full reserve spreads, SoFi’s model targets infrastructure provision where banks, fintechs, and enterprises can issue white-label stablecoins or integrate SoFi rails for instant settlement. Considering they have a Galileo network that already processes billions in annual payment volume, it makes absolute sense.

The GENIUS Act and MiCA created clear compliance frameworks but also substantial barriers to entry because it require capital, legal expertise, and regulatory relationships that established financial institutions already have, and they can enter faster than crypto-native startups.

The GENIUS Act mandates 100% reserves in USD cash or short-term Treasuries (under 93 days), monthly audited public disclosures, and Bank Secrecy Act compliance. Banks can issue through FDIC-approved subsidiaries, while non-banks require OCC approval with substantial capital requirements. For example, SoFi, which fulfills all of these requirements, became the first national bank to issue on a public blockchain. Similarly, 17 EU issuers gained MiCA authorization for 25 E-Money Tokens till November 2025 (14 EUR-pegged, 9 USD-pegged, 1 GBP-pegged, 1 CZK-pegged).

This regulatory complexity serves as a competitive moat for early institutional entrants, and the late entrants must now replicate.

Ripple’s RLUSD ($1.35B market cap) launched in December 2024 with an immediate Mastercard partnership for credit card settlements on XRP Ledger, BNY Mellon custody, and regulatory approvals in the UK, Singapore, Abu Dhabi, and Japan. The integration with ISO 20022 standards via Ripple’s On-Demand Liquidity gave RLUSD the institutional trade finance adoption and also reinforced Ripple’s brand as enterprise blockchain infrastructure.

Let’s take another example of World Liberty Financial’s USD1 ($3.34B market cap). They leveraged their political branding as a differentiation strategy. It was a business venture by the Trump family. With fee-free 1:1 minting/redemption via BitGo Trust custody and deployment across 6 chains (Ethereum, BSC, Tron, Solana, Aptos, Plume), USD1 targets institutional cross-border payments and capitalizes on political alignment. The token reached $2 billion peak volume in December 2025, which could be a great case study to prove that non-traditional branding can drive substantial adoption.

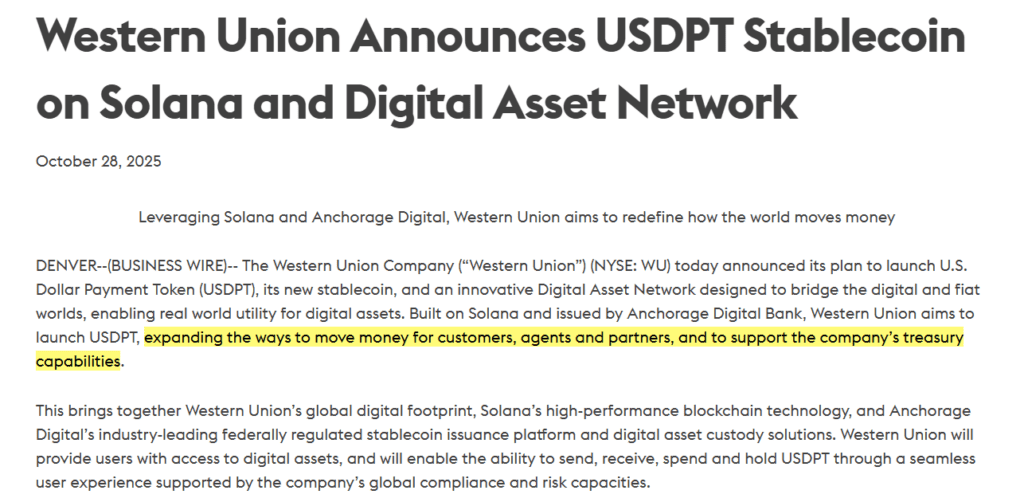

Even traditional remittance providers are entering. Take the example of Western Union. It announced its USDPT stablecoin for launch in H1 2026 on Solana via Anchorage Digital.

These platforms aggregate stablecoin deposits and algorithmically route funds across DeFi protocols for maximum yield, returning profits to users minus management fees.

Morpho, for example, has grown to approximately $13 billion in TVL by pioneering peer-to-peer lending optimization.

Rather than pooling liquidity like traditional protocols, Morpho directly matches depositors with borrowers. For example, when Alice deposits USDC at 3% and Bob borrows at 8%, Morpho connects them directly and splits the 5% spread. This eliminates pooled liquidity inefficiency and delivers 30-40% better rates than Aave or Compound. The protocol’s TVL exploded from $5 billion to $13 billion in 2025, which shows the market demand for sophisticated yield management.

Yearn Finance and Convex Finance complement this ecosystem by auto-compounding yields across multiple protocols. For enterprises holding stablecoins under the GENIUS Act, which prohibits direct interest payments to holders, yield optimizers provide a compliant option to earn 5-12% APY while maintaining liquidity through withdrawal mechanisms that don’t violate regulatory restrictions.

Ondo Finance, which is a Pantera Capital, Coinbase-backed tokenized-RWA platform, has built $1 billion+ TVL by tokenizing U.S. Treasuries into blockchain assets. Users deposit USDC and receive USDY (yield-bearing stablecoin backed by short-term Treasuries) or OUSG (tokenized government bonds), earning 4-5% APY from underlying T-bills while maintaining 24/7 on-chain liquidity.

Ondo captures 0.15-0.30% annual management fees on AUM, generating $1.5-3 million annually from its current scale. The product competes directly with traditional money market funds but settles instantly on-chain, enabling programmable treasury management that legacy systems can’t match.

Their 2025 Recap mentions key collaborations with some of the largest institutions to bring traditional assets onchain

Another example in this category could be Maple Finance, which has $5 billion AUM ($25M ARR) through institutional stablecoin lending pools. Its syrupUSDC product offers corporate borrowers access to stablecoin liquidity at competitive rates while SYRUP token rewards incentivize long-term capital commitment. The platform serves as critical infrastructure for institutions needing dollar-denominated credit without traditional banking friction.

As stablecoin adoption fragments across 50+ blockchains, infrastructure enabling seamless transfers becomes critical.

Across Protocol, which is backed by Paradigm, settles trillions annually using an intent-based architecture. Rather than traditional bridges that pool liquidity and create hacking targets, Across lets users state desired outcomes (e.g., 100 USDC on Arbitrum) while relayers compete to fulfill them. This eliminates bridge hacking risk while enabling instant cross-chain settlement.

Rhino.fi could be another example in this category. They provide API infrastructure for stablecoin bridging and swaps across 35+ chains. The platform serves wallets, exchanges, and DEXs needing cross-chain routing, monetizing through transaction fees and API licensing. As enterprises adopt multi-chain strategies (like USD1’s 6-chain deployment), this middleware layer becomes essential utility infrastructure. They are like Stripe for blockchain payments.

Specialized lending markets for stablecoins optimize interest rates for institutional borrowers and yield-seeking depositors. Aave in this category dominates with around 15B stablecoin supplied and 12B stablecoin borrowed across multiple chains (USDC/USDT represent ~70%). Institutions deposit USDC at 3.4% while borrowers pay 4.6%, with Aave capturing spreads shared with AAVE token stakers.

Stablecoin lending’s competitive advantage stems from lower volatility and enables lower collateral requirements (120% vs. 150%+ for crypto) with predictable interest rates for enterprise treasury planning, and clearer regulatory positioning compared to crypto derivatives. The battle-tested security of protocols like Aave, which has been operating since 2017 without hacks, provides institutional-grade confidence that newer platforms must earn over time.

Ethena’s USDe, which raised $166.5 million (including $100 million private round), pioneered synthetic yield-bearing stablecoins through delta-hedging strategies. Rather than fiat backing, USDe holds crypto (ETH, BTC) while shorting perpetual futures to maintain $1 peg. Funding rate arbitrage between spot holdings and futures positions generates 8-15% APY distributed to USDe holders. The model grew to $6.30 billion market cap in 18 months, which confirms institutional appetite for yield-generating stablecoins that bypass traditional banking.

GAIB is another example here. They combine AI infrastructure financing with stablecoin tokenization. The platform tokenizes GPU leases into AID stablecoin, enabling investors to earn 10-80% yields from GPU rental income demanded by AI training workloads. With $30 million+ in GPU deals financed through stablecoin issuance, GAIB creates a bridge between AI compute demand and DeFi capital markets.

The convergence of AI and stablecoins addresses fundamental needs: autonomous agents require programmable money for microtransactions, stablecoins eliminate FX risk for global agent-to-agent payments, and smart contracts enable autonomous treasury management without human intervention. If AI agent economy has to grow big in 2026, stablecoins have to be the native payment rails.

Traditional payment processors are integrating stablecoin settlement to capture efficiency gains and network fees. Visa’s USDC settlement for U.S. banks on Solana (launched December 2025) achieved $3.5 billion annualized volume in initial months with Cross River and Lead Bank.

The infrastructure enables real-time 24/7 settlement versus traditional 7-day batch windows, with Solana chosen for sub-second finality and low transaction costs. Visa captures network fees on settlement volume while modernizing treasury operations for partner institutions.

Stripe processed $5.7 trillion in stablecoin flows in 2025 after launching subscription payments on Polygon with 113 active merchants generating $8-9 million monthly peaks. The company acquired Bridge (stablecoin infrastructure provider) to control the full stack, enabling merchants to hold stablecoin balances and reduce forex exposure. Stripe’s Financial Accounts product now operates in 101 countries, positioning stablecoins as a global payment infrastructure rather than crypto-native tools.

Mastercard-Thunes partnership enables stablecoin wallet payouts to 10 billion endpoints across 130 countries, focusing on remittance and cross-border flows. The infrastructure charges per-transaction routing fees while competing directly with legacy SWIFT rails that take 3-5 days and cost 3-7% in fees.

Analysis of current gaps and emerging trends reveals the highest-potential opportunities for founders entering the stablecoin space.

1. Compliant Yield-Bearing Enterprise Stablecoins.

The GENIUS Act prohibits direct interest payments on stablecoins, yet enterprises managing $500+ billion in corporate cash need yield on treasury balances with daily liquidity. The solution: tokenize T-bill and MMF portfolios into yield-bearing instruments with instant redemption to USDC/USDT via automated market makers. Something like Ondo.

The market can support 10+ specialized providers across different verticals—corporate treasury, family offices, pension funds, endowments—each with unique compliance needs and yield preferences.

2. Privacy-Preserving Stablecoin Infrastructure

Enterprises won’t use transparent public blockchains for B2B payments because they expose supplier relationships, pricing strategies, and working capital positions to competitors. The $120 trillion annual enterprise B2B payment market demands privacy, yet regulatory compliance requires selective disclosure to authorities.

Building on privacy chains like Aleo (which Circle chose for USDCx offering banking-level privacy) or integrating zero-knowledge proofs (like ZKsync chains) on chains enables compliant confidential transactions. The architecture will maintain regulatory compliance through selective disclosure. Regulators will see full transaction details while the public sees encrypted commitments.

3. Multi-Currency Stablecoin Exchange Infrastructure

Approximately 95% of stablecoins are USD-pegged, yet international trade demands EUR, GBP, JPY, and emerging market currencies. But there is a gap for an optimized exchange infrastructure for stablecoin FX swaps.

Building FX-optimized DEXs for stablecoin pairs (USDC/EURC/GBPC swaps) targeting the $7.5 trillion daily FX market with 24/7 atomic settlement captures inefficiencies in legacy systems.

4. Stablecoin Payment APIs for AI Agents

AI agents need programmable payment rails for autonomous transactions. Credit cards and ACH don’t work for machine-to-machine economies. Building API platforms enabling AI agents to hold and send stablecoins with built-in compliance (transaction limits, recipient screening) integrated with major AI frameworks (OpenAI, Anthropic agents) positions providers as infrastructure for emerging agent economies.

Use cases span AI agents paying for compute and data autonomously, automated supply chain payments triggered by IoT sensors, and microtransactions for content and API usage between agents. Revenue models combine 0.5-1% transaction fees with SaaS subscriptions for API access.

5. Stablecoin-Collateralized Credit Products

Traditional banks won’t lend against crypto assets, yet stablecoin holders want leverage without selling positions. Institutional lending using stablecoins as collateral with lower loan-to-value ratios (80-90% vs. 50% for volatile crypto) serves businesses holding operational stablecoin balances needing working capital.

While Maple Finance focuses on institutional unsecured lending, secured stablecoin lending remains underserved. Real-world identity verification and legal recourse frameworks provide downside protection missing in pure DeFi protocols.

6. Regulatory Compliance Infrastructure (Compliance-as-a-Service)

The GENIUS Act and MiCA require monthly audited disclosures, reserve proofs, and KYC/AML integration—expertise most startups lack. White-label compliance stacks that enable automated reserve attestations, regulatory reporting, and KYC integration empower smaller issuers to launch compliant regional or industry-specific stablecoins.

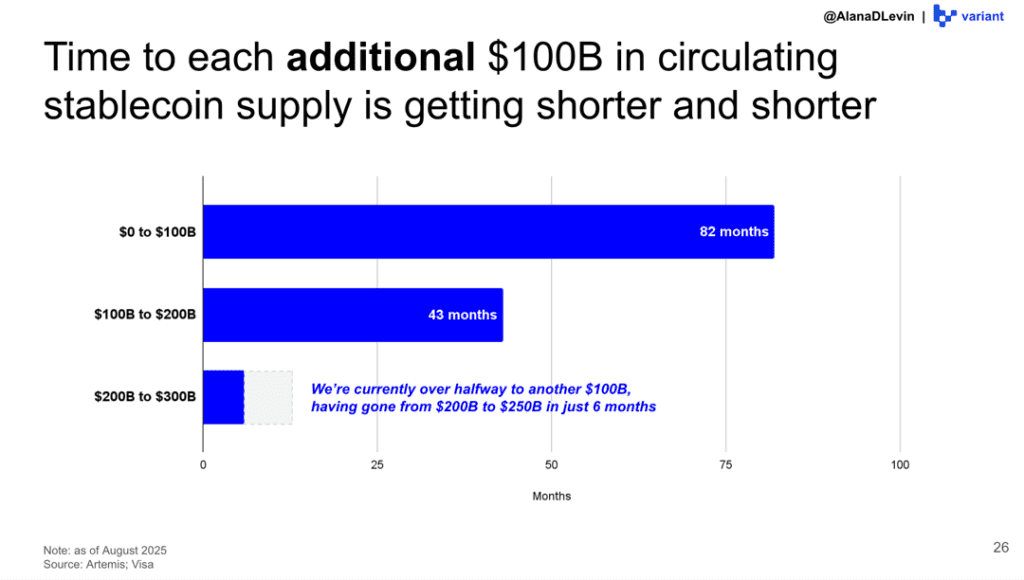

The stablecoin market is heading to ~$1.6T by 2030 and the time to add an additional 100B in Stablecoin supply is getting shorter and shorter.

If you are planning to build/ building anything around Stablecoins, Prolitus can help you with smooth technical execution/development with regulatory readiness.

Why partner with Prolitus?

Partner with a team that has delivered over 200 global projects in the last 10 years. Schedule a call with us to discuss your requirements.